Key Takeaways:

- Average monthly student loan payment is around $500, but varies by loan type.

- Federal undergraduate loans have 6.53% interest; graduate and PLUS loans up to 9.08%.

- Loan payments depend on degree type, with medical students facing the highest amounts.

- Income-driven repayment (IDR) plans base payments on income, potentially lowering them.

How Much Are Student Loan Payments?

The average repayment amount for student loans is $500 monthly.

This reflects the average student loan debt payments and median salaries of college graduates, but depending on your situation and other economic factors, you can pay more or less.

To give you specific information on student loan payments, we’ve gathered updated data for public and private student loans disbursed in the 2024/2025 academic session. Keep reading to find out more.

Comparison of Monthly Payments by Loan Type

Your payments can be slightly higher or lower depending on the type of loan. Undergraduates generally pay less for federal loans than graduate and PLUS loans.

Federal Undergraduate Subsidized/Unsubsidized Loans

The interest rate for undergraduate federal student loans is 6.53% per year. This rate applies to loans disbursed between July 1, 2024, and June 30, 2025.

| Loan Amount ($) | Monthly Payments at 6.53% for 10 years |

| 5,000 | $56.86 |

| 10,000 | $113.72 |

| 15,000 | $170.58 |

| 20,000 | $227.44 |

| 25,000 | $284.30 |

| 30,000 | $341.16 |

| 35,000 | $398.01 |

| 40,000 | $454.87 |

Federal student loan borrowers can expect a repayment period of 10 years under the standard plan, while other options, like income-driven repayment plans, may offer lower payments over extended terms.

Federal Graduate Subsidized/Unsubsidized Loans

The interest rate for federal graduate loans in the 2024-2025 academic year is 8.08%. Unlike undergraduate loans, graduate borrowers are only eligible for unsubsidized loans, meaning interest begins accruing as soon as the loan is disbursed.

However, the interest rate remains fixed for the life of the loan, ensuring stable monthly payments.

| Loan Amount ($) | Monthly Payments at 9.08% for 10 years |

| 5,000 | $60.88 |

| 10,000 | $121.77 |

| 15,000 | $182.65 |

| 20,000 | $243.53 |

| 25,000 | $304.42 |

| 30,000 | $365.30 |

| 35,000 | $426.18 |

| 40,000 | $487.07 |

Federal Plus Loans

PLUS loans are offered to graduate students and parents of dependent undergraduate students to help cover the cost of education not covered by other financial aid.

Compared to other federal loans, they require a credit check.

| Loan Amount ($) | Monthly Payments at 9.08% for 10 years |

| 5,000 | $60.88 |

| 10,000 | $121.77 |

| 15,000 | $182.65 |

| 20,000 | $243.53 |

| 25,000 | $304.42 |

| 30,000 | $365.30 |

| 35,000 | $426.18 |

| 40,000 | $487.07 |

For the 2024-2025 academic year, the interest rate for federal PLUS loans is 9.08%. While this rate is higher than the rest, it’s often used to fill gaps in financing educational costs.

Like graduate loans, PLUS loans do not receive subsidies. Borrowers are responsible for all interest charges during school, grace periods, and deferment periods.

The repayment term usually ranges from 10 to 25 years without a borrowing cap. This makes them a suitable option for those who need significant financial assistance.

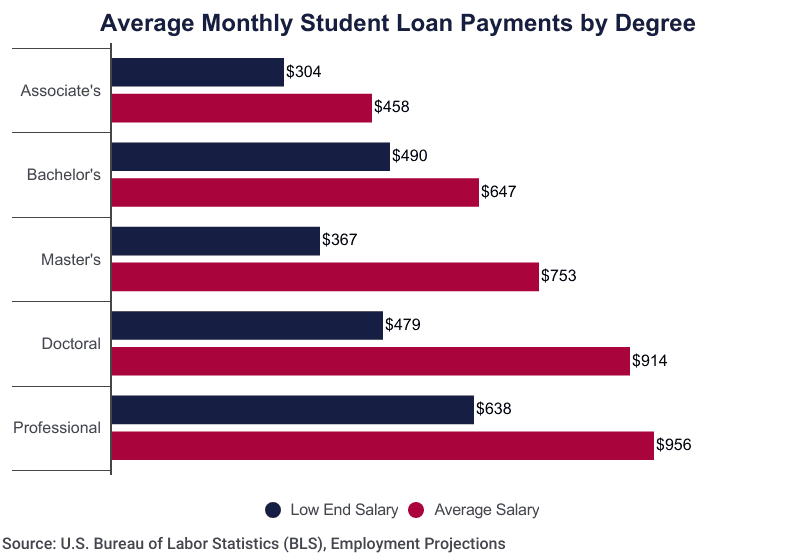

Average Monthly Payments by Degree Type

Different degree types might have varying interest rates due to differences in borrowing limits, education costs, and loan terms.

Associate’s Degree

Borrowers with an associate degree usually have lower student debt than those with bachelor’s or graduate degrees. Depending on the loan amount and repayment plan, the average student loan payment per month is estimated to be around $100 to $400.

Associate degrees typically have shorter durations and lower overall costs, resulting in lower monthly payments.

Bachelor’s Degree

The average monthly payment for graduates with a bachelor’s degree is around $300 to $500.

Most students take out $28,000 to $30,000 in loans for a four-year degree, leading to a standard monthly payment of approximately $300 on a 10-year repayment plan.

Graduate Degree (Master’s, PhD, etc)

Graduate students, particularly those pursuing master’s or doctoral degrees, can expect to pay more. Graduate degrees have extended study periods, which also means higher costs.

Monthly payments for graduate degree holders can range between $400 and $1,000. For instance, a borrower with $50,000 in graduate loans at 8.08% would pay about $600 per month on a 10-year plan.

Average Monthly Payments For Medical School Debt

Student loans for professional degrees like medicine have the highest average monthly payments due to the substantial cost of education. As a graduate here, you may accumulate between $200,000 and $300,000 in student loan debt, depending on whether you attend a public or private school.

Let’s say you take out a federal student loan at a fixed interest rate of 6.53%. Using a standard 10-year repayment plan, your monthly payments can range from $2,269 to $3,500.

The thought of these rates and potential repayment amounts as a medical student can be overwhelming. But, thankfully, you can get support from experts like Student Loan Professor to help you navigate better options for lower payments.

For instance, IDR plans tie your monthly payments to income. Under these circumstances, your monthly payments can be significantly lower– sometimes as low as $500 to $1,000.

IDR Plan Monthly Payments Based on Income

Income-driven repayment (IDR) plans are designed to make student loan payments more manageable by adjusting them according to a borrower’s income and family size.

These plans cap monthly payments around 10% to 20% of the borrower’s discretionary income, with remaining balances forgiven after 20 to 25 years of qualifying payments.

Although IDR plans have appealing benefits, several loopholes can complicate things for borrowers.

For instance, the IRS might consider any remaining loan balances that are forgiven at the end of the repayment period as taxable income. This creates a significant tax liability for borrowers (tax bomb).

Additionally, eligibility rules and recertification requirements often change. The only way to stay updated with these changes or navigate through the complex processes is through the help of an expert.

How to Calculate Your Student Loan Payments

Learning to calculate your student loan payments is an essential part of the loan process. First, it helps you stay organized and prepare financially.

Thankfully, you can find a student loan payment calculator on the Internet—your lender might even have one on its site.

However, it also helps to know how these calculations work manually.

To calculate your student loan payments, you’ll need to know your:

- Loan amount

- Interest rate

- Repayment term

Standard Repayment Formula

The formula for calculating monthly payments on a standard loan (with fixed payments) is:

M = [ P×r×(1+r)n ] ÷ (1+r)n−1

Where:

- M is the monthly student loan payments

- P is the loan principal

- r is the monthly interest rate (annual interest rate divided by 12)

- n is the total number of payments (loan term in months)

Example:

If you borrowed $30,000 at an interest rate of 6.53% over 10 years, your monthly interest rate would be 0.0653÷12= 0.00544. For a 10-year term, there are 120 months of payments.

Plugging this into the formula gives:

M= [30,000 x 0.00544 x (1 + 0.00544)120] ÷ (1 + 0.00544)120 – 1)

M= $341.16

So your monthly payment would be about $341.16

Income-Driven Repayment Plan Calculation

If you’re on an IDR Plan, your monthly payments are based on your discretionary income rather than the loan amount. Discretionary income is usually defined as the difference between your adjusted gross income (AGI) and the 150% of the federal poverty line for your family size and state.

Example:

If your AGI is $50,000 and you have a family of four, the Federal poverty guideline might be around $30,000. So, your discretionary income would be $50,000 – $30,000= $20,000.

If your plan requires 10% of discretionary income, your monthly payment would be:

(0.10 x 20,000) ÷ 12= $165.67

Lower Your Monthly Payments with Student Loan Professor

From this article, you’ve learned that your monthly payment can depend on several conditions, including your type of loan, repayment plan, or even educational level.

We’ve also seen that medical students can expect to pay quite high monthly fees. However, you can manage these payments with the right help.

At Student Loan Professor, we have a team of experts who have been where you are and have learned through experience how to navigate your current situation and reduce your monthly payments.

Check out our services to learn more.

Brandon Barfield is the President and Co-Founder of Student Loan Professor, and is nationally known as student loan expert for graduate health professions. Since 2011, Brandon has given hundreds of loan repayment presentations for schools, hospitals, and medical conferences across the country. With his diverse background in financial aid, financial planning and student loan advisory, Brandon has a broad understanding of the intricacies surrounding student loans, loan repayment strategies, and how they should be considered when graduates make other financial decisions.